A new congressional report finds overpayments to Medicare Advantage (MA) plans are raising Part B premiums for all beneficiaries, accounting for $82 billion in additional premiums over the past ten years. Produced by the Senate Joint Economic Committee (JEC), the brief examines these burdens and opportunities for reform.

Key findings include:

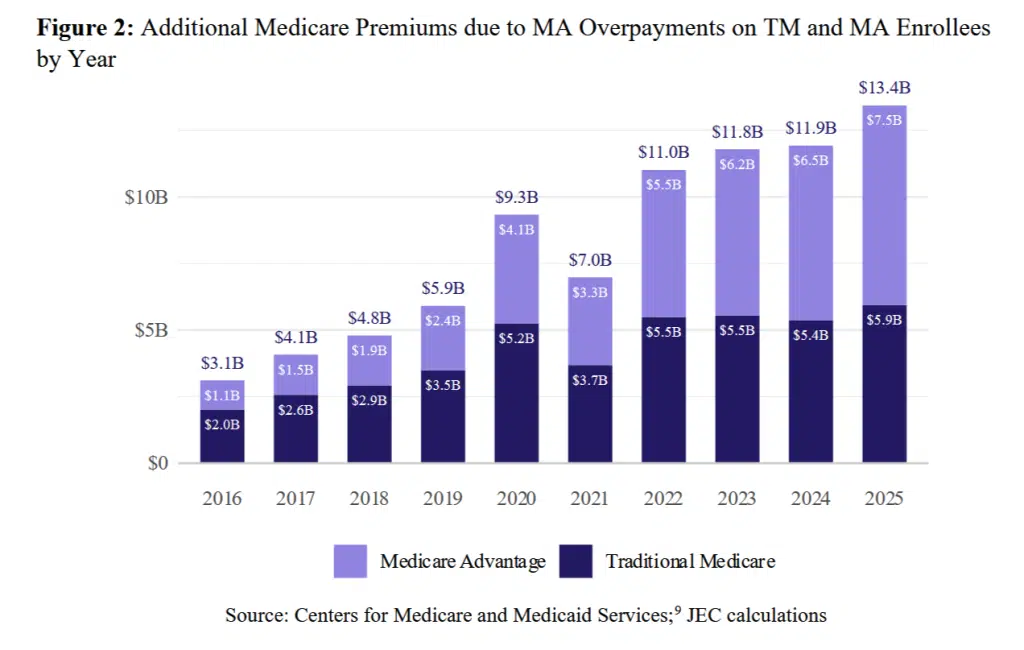

Overpayments increase premiums for all beneficiaries—not just MA enrollees. In 2025, MA overpayments drove up Part B premiums by $212 per person, for a total of $13.4 billion. People with Original Medicare (OM), who do not have access to the supplemental benefits that most MA plans offer, bore roughly $6 billion of that burden.

Taxpayers are also affected. Medicare enrollees pay for about 85% of the added premium costs, with the remainder falling on federal (9%) and state (6%) taxpayers.

This is a long-standing issue. Despite promises that MA would save Medicare money, it never has. Since 2016, MA overpayments have added $82 billion to Part B premiums.

Higher premiums mean lower Social Security checks. Since most beneficiaries (nearly 70%) have their Part B premiums withheld from Social Security checks, any premium increases directly reduce their benefits.

Absent reforms, overpayments will continue to spike premiums. Annual Part B premiums are expected to double between 2025 and 2035, growing from roughly $2,440 to $5,000. If MA continues to be paid at 120% of OM, the additional per-beneficiary premium burden would rise from $212 to $450 over the same period.

Corrections are needed. The JEC recommends aligning MA payments with OM to “prevent unnecessary premium growth, increase the affordability of Medicare, and protect net Social Security checks.”

MA’s Unmet Promise

Private MA plans contract with Medicare to provide Part A (Hospital Insurance) and Part B (Medical Insurance) benefits; they also typically offer supplemental benefits not available to people with OM.

The original intent of MA was to generate savings, a goal it has yet to realize.

The JEC report acknowledges the original intent of MA was to generate savings, a goal it has yet to realize. In addition to this historical context, its authors make future projections based on then-current (March 2025) data from the non-partisan Medicare Payment Advisory Commission (MedPAC), which estimated MA costs would be about 20% higher than OM in 2025, resulting in $84 billion in overpayments. A subsequent MedPAC analysis put that estimate closer to $76 billion.

JEC defines overpayments in this context as “how much higher MA payments are, on average, relative to [O]M for the same beneficiaries.”

MA Overpayments and Part B Financing

Medicare Part B is financed through the Supplementary Medical Insurance (SMI) Trust Fund, which relies on a combination of beneficiary premiums and transfers from the general fund. Each year, Part B premiums are set to cover 25% of expected costs; some people pay more, based on income. As the report notes, “A key aspect of this financing mechanism is that while the standard Part B premium varies with income, it does not vary based on whether the individual receives Part B benefits” through OM or MA. In other words, and as the chart below illustrates, everyone—regardless of the coverage pathway they choose—is on the hook for excess payments to MA plans.

An accompanying press release explains it further: “In 2025, covering a beneficiary in MA cost an estimated 17 to 20 percent more on average than it would have cost in [O]M. MA overpayments raise Part B spending, and because premiums are set to cover roughly one-quarter of expected costs, premiums for everyone in Part B increase.”

Affordability Impacts

MA overpayments make Medicare Part B less affordable. In addition, people with Medicare are particularly affected by Part B spending growth, which JEC notes is on the rise:

“Over the next decade, per-person Part B expenditures are projected to nearly double, from around $9,100 in 2025 to over $18,000 in 2035. Because the standard Part B premium is set to cover 25 percent of expected costs, baseline premiums are expected to nearly double as well, from about $2,200 per year in 2025 to about $4,500 in 2035. Average premiums are expected to grow even more. Under these projections, premiums will rise sharply for seniors who rely on Medicare.”

Part B spending influences how much enrollees pay for care.

Beyond premiums, Part B spending influences how much enrollees pay for care. For example, under Medicare cost-sharing rules, beneficiaries are generally required to cover 20% of Part B services. When those services become more expensive, beneficiary pocketbooks take a direct hit.

Ever-higher costs can have an outsized effect, as many beneficiaries rely on fixed or limited incomes that cannot keep pace: Half of all beneficiaries, nearly 33 million people, live on $43,200 or less per year, and one quarter have less than $18,950 in savings. If costs continue to climb as anticipated, more and more people could be forced to make impossible choices, like paying their doctor or paying their rent.

Conclusion

Looking ahead, the JEC concludes it is“imperative for policymakers to act to prevent premiums from gradually eating away at seniors’ social security checks.” They note that MA overpayments “are not inevitable. They ultimately result from a policy choice to pay more for Medicare Advantage than for Traditional Medicare. Aligning Medicare Advantage payment levels with Traditional Medicare would directly limit this avoidable premium growth and protect the Social Security benefits of 50 million Part B beneficiaries. Reform that gradually achieves payment parity could save each senior approximately $2,600 over the next decade.”

MA overpayments “result from a policy choice to pay more for Medicare Advantage than for Traditional Medicare.”

Medicare Rights agrees reforms are needed to improve MA payment accuracy, beneficiary health and financial security, and Medicare sustainability. Despite promises that MA would save Medicare money, it never has. The current system rewards insurers with greater profits but penalizes all beneficiaries through higher Part B premiums and taxpayers through increased costs. Absent corrections that center beneficiary needs, these impacts will only deepen.

For More Information

Read the report, The Part B Premium Pass Through: Medicare Advantage Overpayments Inflate Premiums for All.

The JEC released a companion analysis, the Medicare Affordability Tracker, which quantifies how overpayment-driven premium burdens at the state and congressional district levels.

Senate Finance Committee Members Introduce Bill to Reduce Medicare Out-of-Pocket Costs, Improve Access to Medicare Savings Programs

Senate Finance Committee Members Introduce Bill to Reduce Medicare Out-of-Pocket Costs, Improve Access to Medicare Savings Programs  H.R. 1 Funding Cuts Jeopardize State Economies

H.R. 1 Funding Cuts Jeopardize State Economies - Accuracy, Accountability, and Accessibility Vital for Good MA Provider Directories

- Medicare Advantage Organizations Reap Ever Larger Bonuses

2 Comments on “Congressional Report Details How MA Overpayments Drive Up Part B Premiums”

Jonathan Paddon

March 13, 2026 at 1:50 amIt all depends on how you frame it. You can say that Medicare Advantage gets overpaid or you can say that original Medicare skimps on benefits. Is it really overpayment if Medicare Advantage has objectively richer benefits than original Medicare? And if you deny that Medicare Advantage has objectively richer benefits, then why doesn’t original Medicare immediately implement a maximum out of pocket for all beneficiaries? How much would that cost? A lot more than the so-called overpayment cited by this article. Yet this is just one of the valuable benefits that Medicare Advantage already provides that original Medicare lacks. Yes, someone can purchase a Medicare supplement to acquire this cost protection. But then you should include the cost of supplemental coverage in your analysis!

Also, why don’t you consider the many instances of fraud in original Medicare that don’t happen in Medicare Advantage because the insurance companies provide better oversight of claims. Look at the well-publicized cases of fraudulent billing for COVID tests and urinary catheters to the tune of billions of dollars, to name but two recent examples.

The article suggests that it is not fair for those on original Medicare to pay more for benefits that they are not receiving. But that is their choice. They have made a decision that the freedom from networks and prior authorizations that they get with original Medicare is worth forgoing the benefits that they would receive on Medicare Advantage such as a maximum out-of-pocket limit on yearly costs and things like dental and vision coverage. Others make the opposite choice and we should be thankful that we have a system that provides various options according to people’s different needs and preferences.

Medicare Advantage is certainly not for everyone and is far from perfect. Insurance companies have been rightly criticized for inflating risk adjustment scores by identifying questionable diagnoses in members to increase payments from the government. Increased oversight is certainly warranted. But any comparison of Medicare Advantage and Original Medicare should consider both costs and benefits and not costs alone.

Those who focus on cost alone are pushing a political agenda to try to eliminate any role for the insurance companies and force all Medicare beneficiaries onto a one-size fit’s all solution where everyone would have to be on original Medicare.

Medicare Rights Center

March 13, 2026 at 3:56 pmThank you for your thoughtful engagement. While Medicare Advantage plans may in theory offer richer benefits, there are many questions left unanswered about the utilization and accessibility of these benefits. On paper, they can help meet gaps left in Original Medicare, but lived experiences, including the experiences we hear on our national helpline, indicate that plans cannot or will not follow through on some marketed offerings, or that eligibility for supplemental benefits is more restrictive than initially understood.

Right now, as you point out, choosing a Medicare pathway is a trade-off between many factors, often weighing things like supplemental benefits vs. freedom of choice of provider, or out-of-pocket maximums vs. prior authorizations. We strive towards a program where such trade-offs are better understood and that the final choice does not leave any Medicare beneficiary struggling to afford their care.

Closing coverage gaps between Original Medicare and Medicare Advantage, including by incorporating dental, vision, and hearing coverage in Original Medicare, would provide more standard benefits in support of all beneficiaries’ whole-body health and financial security.

You may be interested in some of our other resources on the topic of supplemental benefits, linked below.

https://www.medicarerights.org/policy-documents/beneficiary-experiences-with-medicare-advantage-supplemental-benefits

https://www.medicarerights.org/policy-documents/filling-gaps-in-medicare-coverage-dental-vision-and-hearing

https://www.medicarerights.org/medicare-watch/2025/06/26/medicare-advantage-enrollees-need-better-information-on-supplemental-benefits